Figuring out who is on the hook for money owed when you are married can feel a bit like trying to solve a puzzle. It's a question many folks think about, and for good reason, too. When you tie the knot, you often blend lives, and that includes finances, in a way. Yet, the rules about debt don't always follow a straight line across the country, which is interesting, actually.

It's not just about what you or your partner spent; it's also about where you live, you know? The laws from one state to the next can be really different when it comes to shared financial obligations. What might be true for someone living in California, for example, could be quite unlike the situation for a couple in New York. This makes understanding the specifics for your own area very important, and it's something many people wonder about, certainly.

So, if you're asking, "In what states are you responsible for your spouse's debt?", you're asking a really smart question. It shows you're thinking ahead about your financial well-being, and that's a good thing. We're going to explore the various ways different parts of the United States handle this shared money matter, giving you a clearer picture, hopefully, of what you might need to know today.

Table of Contents

- Understanding the Basics of Spousal Debt

- Community Property States: The Shared Financial Path

- Common Law States: Individual Responsibility

- Exceptions and Special Situations

- Steps to Take for Your Financial Peace of Mind

- Frequently Asked Questions About Spousal Debt

Understanding the Basics of Spousal Debt

When we talk about who owes what in a marriage, it's not always simple. The main idea is that some states see marriage as a partnership where almost everything, including debts, gets shared. Other states tend to keep things more separate, treating each person's debt as their own, you know? This difference is pretty big and affects a lot.

It's interesting how the legal systems in the United States, with its 50 states, have developed such different approaches to this. Each of the 50 states has its own way of looking at married couples' finances. This means that if you move from one state to another, the rules about your spouse's debt might change, which is something to keep in mind, really.

Knowing these basic differences helps you figure out your own situation. It's about understanding the big picture before we get into the details of specific state rules. So, let's look at the two main ways states handle this, which are quite distinct, as a matter of fact.

Community Property States: The Shared Financial Path

In certain parts of the country, a marriage is seen as a joint economic venture, where both people own everything equally that they get during their time together. This includes not just money and things, but also debts. These are known as "community property" states, and their way of doing things is based on a long history, typically.

This idea means that if one person takes on a debt while married, for the benefit of the family or the marriage, that debt is often considered to belong to both of them. It's a shared responsibility, even if only one name is on the credit card or loan papers. This can be a bit surprising for some people, naturally.

So, if you live in one of these states, you could be responsible for a debt your partner took on without your direct involvement. It's a system that emphasizes the shared nature of marriage, in a way, which is a key part of their legal framework, obviously.

What is Community Property Debt?

Community property debt is money owed that was taken on by either spouse during the marriage, for the benefit of the marriage or the family unit. This could be anything from a car loan for family transportation to medical bills for a child, or even credit card debt used for household expenses, you know?

It doesn't matter whose name is on the loan document or credit card. If the debt was incurred while you were married and for a purpose that benefits the community (meaning, the married couple), it's generally considered community debt. This can be a big difference from what some people expect, quite often.

There are some exceptions, though. Debts taken on before the marriage, or debts that were clearly for one person's sole benefit and not the family, might be considered separate debt. But the general rule is that if it happened during the marriage and served the couple, it's shared, basically.

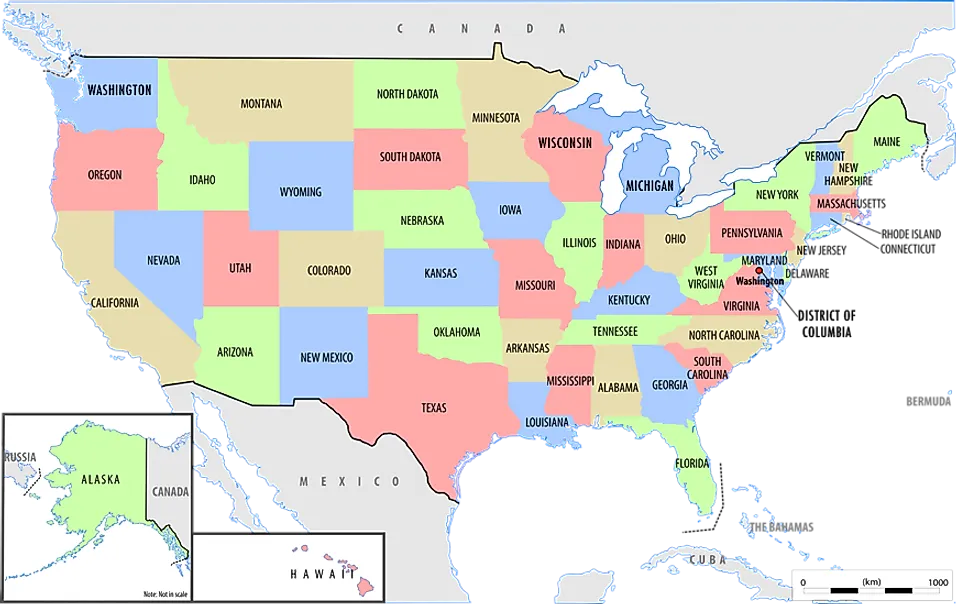

The Community Property States List

There are nine states in the United States that follow community property laws. These states have a distinct approach to how assets and debts are divided when a couple gets divorced or when one spouse passes away. It's a pretty specific list, and it's good to know if your state is on it, certainly.

Here are the community property states:

- Arizona

- California

- Idaho

- Louisiana

- Nevada

- New Mexico

- Texas

- Washington

- Wisconsin

Additionally, Alaska allows couples to opt into a community property system through a special agreement, which is a unique twist. And Puerto Rico, a U.S. territory, also follows community property principles. So, if you're in one of these places, the rules about shared debt are likely to apply to you, typically.

Common Law States: Individual Responsibility

Most states in the United States operate under what's called "common law" when it comes to property and debt in a marriage. This system is quite different from community property. Here, generally speaking, what's yours is yours, and what's your spouse's is theirs, financially speaking, that is.

In common law states, if one person takes on a debt, that debt usually belongs only to that person. Their spouse is not automatically responsible for it, even if they are married. This offers a bit more individual financial separation within the marriage, which some people prefer, obviously.

This means that if your partner gets a credit card in their name only, and runs up a balance, you generally won't be on the hook for that debt. Creditors would typically go after the person whose name is on the account. It's a pretty straightforward idea, in some respects.

How Common Law States Handle Debt

In common law states, the general rule is that debt follows the person who incurred it. If you sign for a loan, it's your loan. If your spouse signs for a loan, it's their loan. This holds true for most types of debt, like credit cards, car loans, or personal loans, you know.

However, there are important exceptions to this general rule. Just because a state is a common law state doesn't mean you're completely shielded from your spouse's financial troubles. For instance, if you co-sign a loan with your partner, then you are both equally responsible for that debt, which makes sense, really.

Also, if you have a joint bank account and your partner uses it to incur debt, or if you both use a credit card that's in both your names, then you are both liable. It's about whose name is on the agreement, and whether the debt was taken on jointly, so that's a key point, certainly.

Exceptions and Special Situations

Even with the clear differences between community property and common law states, there are always some situations that don't fit neatly into one box. Legal matters, especially around money and marriage, can have their own twists and turns. It's important to know about these special cases, too, as a matter of fact.

These exceptions can sometimes change who is responsible for a debt, regardless of whether you live in a community property or common law state. It's not always as simple as "my debt" or "our debt." There are nuances that can shift the responsibility, which is why it's good to be informed, naturally.

Understanding these particular circumstances can help you protect your own financial future. Let's look at some of the common exceptions and special rules that might affect who pays what, because they can make a big difference, obviously.

Jointly Held Accounts and Loans

This is a big one, and it applies everywhere, in all 50 states, no matter their specific property laws. If you and your spouse both put your names on a loan, a credit card, or any other financial agreement, then you are both equally responsible for that debt. It's a shared promise to pay, essentially.

When you co-sign for something, you're telling the lender that if one person can't pay, the other person will. This means your credit can be affected if payments are missed, even if you weren't the one who made the purchases or used the money directly. It's a very clear commitment, typically.

So, before you put your name on any joint account or loan with your partner, make sure you understand the full responsibility you're taking on. It's a shared burden, and it's something to think about carefully, you know, before signing on the dotted line.

The Necessaries Doctrine

This old legal idea, often called the "necessaries doctrine," is still around in many states, both common law and community property. It says that one spouse can be held responsible for the other spouse's debt if that debt was for "necessaries." These are things essential for living, like food, shelter, clothing, or medical care, basically.

The idea behind this is that married couples have a duty to support each other. So, if one spouse gets medical treatment, for example, and can't pay, the other spouse might be required to pay for it, because medical care is considered a necessary item. This applies even if only one person's name is on the bill, which is interesting, actually.

The definition of "necessaries" can vary a bit from state to state and even depend on the couple's lifestyle. But the core idea is that basic living expenses for the family are often a shared responsibility, regardless of who incurred the debt, in a way.

Pre-Nuptial and Post-Nuptial Agreements

For couples who want to define their financial responsibilities more clearly, especially regarding debt, a pre-nuptial agreement (before marriage) or a post-nuptial agreement (after marriage) can be a powerful tool. These are legal papers that lay out how assets and debts will be handled, which is very helpful, certainly.

These agreements can specify that certain debts remain the sole responsibility of one spouse, even in community property states. They can protect one person from debts incurred by the other, or clarify who owns what if the marriage ends. It's a way for couples to create their own financial rules, essentially.

However, these agreements must be properly written and signed to be legally binding. It's always a good idea to have a legal professional help you with these, so they hold up in court if needed. They offer a lot of control over your financial future, obviously.

Debt Before the Wedding

Generally speaking, debts that one person brings into the marriage are considered their separate debt. This means that if your partner had student loans or credit card debt before you got married, you are typically not responsible for paying those off. This is true in both common law and community property states, which is good news for many, really.

The key here is when the debt was taken on. If it was before the marriage, it's usually seen as belonging to the individual. Marriage doesn't automatically transfer pre-existing debt to both partners. This provides a clear boundary for financial obligations, in some respects.

However, if separate debt is "commingled" with marital assets—for example, if a joint account is used to pay off a pre-marital loan—things can get a little more complicated. But the general rule is that what's yours before the "I do's" stays yours, typically.

Debt from Wrongful Acts

If a debt arises because one spouse committed a wrongful act, like fraud or a crime, the other spouse is generally not responsible for that debt. This is true in most places, regardless of community property or common law rules. It's about personal accountability, essentially.

For example, if one spouse commits a crime and is ordered to pay fines or restitution, those debts typically fall only on the person who committed the act. The innocent spouse is usually not on the hook for such obligations. This protects people from being penalized for their partner's bad choices, which makes sense, certainly.

This area can get complex, though, especially if marital funds were used in the wrongful act. But the general principle is that debts from individual wrongdoing are usually not shared by the other spouse, you know, which provides a measure of fairness.

Steps to Take for Your Financial Peace of Mind

Understanding these laws is a great first step, but what can you actually do to protect yourself and your family's money? Being proactive is key, especially today with all the different financial products out there. It's about open talks and smart choices, really.

First, have honest conversations with your spouse about money. Talk about your debts, your income, and your financial goals. This kind of open communication can prevent many problems down the road. It's a very important foundation, typically.

Second, be careful about co-signing loans or opening joint accounts. Remember, when you put your name on something with your spouse, you are taking on equal responsibility. Think about the implications before you agree, you know.

Third, consider a pre-nuptial or post-nuptial agreement if you have significant separate assets or debts, or if you simply want clear boundaries. These legal papers can provide a lot of clarity and protection. They are a valuable tool for many couples, certainly.

Fourth, keep an eye on your credit report regularly. This helps you spot any debts that might appear unexpectedly or accounts opened without your knowledge. It's a good habit for anyone, married or not, honestly.

Finally, if you have specific questions about your situation, especially if you live in one of the community property states or have complex financial matters, it's always a good idea to speak with a legal professional who knows about family law or debt. They can give you advice tailored to your unique circumstances. You can learn more about financial planning on our site, and for details on state-specific laws, you can find more information here, as a matter of fact. A reputable legal resource can offer more general guidance on these matters, too.

Frequently Asked Questions About Spousal Debt

What is community property debt?

Community property debt is any money owed that either spouse took on during the marriage, and it was generally for the benefit of the married couple or the family. This means it's considered a shared financial obligation, even if only one person's name is on the original loan or credit card agreement, you know. It's a core idea in specific states that see marriage as a joint economic venture, essentially.

What is separate property debt?

Separate property debt is money owed that belongs solely to one spouse. This usually includes debts incurred before the marriage, like student loans or credit card balances from before the wedding day. It can also include debts incurred during the marriage but specifically for one person's benefit and not for the family, or debts from a wrongful act. In common law states, most debts are considered separate unless they are jointly signed, which is a key difference, certainly.

Can I be sued for my spouse's debt?

Yes, you can be sued for your spouse's debt, but whether you are held responsible depends on several factors. If you live in a community property state, or if you co-signed for the debt, or if the debt falls under the "necessaries doctrine," you could be held liable. In common law states, it's less likely unless you are a co-signer or the debt is for essential family needs. It's a complex area, so understanding your state's specific rules is really important, naturally.

Detail Author:

- Name : Elton Rippin

- Username : tstreich

- Email : oscar.hane@torphy.com

- Birthdate : 2001-05-27

- Address : 21614 Lockman Corners North Jovanyland, MD 03614

- Phone : +1-234-584-5719

- Company : Volkman, Roob and Jenkins

- Job : Movers

- Bio : Sapiente natus nemo numquam sit. Dolores commodi est amet explicabo atque aut eum. Consequatur occaecati eligendi iure ratione quidem.

Socials

tiktok:

- url : https://tiktok.com/@millsg

- username : millsg

- bio : Harum saepe rerum dicta minus voluptatum fuga neque.

- followers : 4684

- following : 643

linkedin:

- url : https://linkedin.com/in/gracemills

- username : gracemills

- bio : Sunt voluptas quas laborum qui ad.

- followers : 4507

- following : 1627

instagram:

- url : https://instagram.com/grace_mills

- username : grace_mills

- bio : Praesentium iure quos ratione perferendis voluptatum id quos. Nam expedita est autem.

- followers : 3516

- following : 2771

facebook:

- url : https://facebook.com/grace_mills

- username : grace_mills

- bio : Ad error voluptatem alias voluptate iure suscipit aut.

- followers : 2059

- following : 917

twitter:

- url : https://twitter.com/grace6392

- username : grace6392

- bio : Delectus perspiciatis dolor occaecati aut velit ut. Occaecati illo esse quia. Dolores nemo accusantium et et.

- followers : 480

- following : 1006